TP qube

Welcome to our article on a crucial transfer pricing issue: intragroup loans.

Intragroup loans raise significant transfer pricing concerns, and, in this article, we will explore the following questions:

- Back to basics, what are intragroup loans?

- What are the main transfer pricing questions raised by intragroup loans?

- Which transfer pricing methodology should I use to document intragroup loans?

- How should arm’s length interest rates be computed?

- As a taxpayer, how can I document my transfer pricing policy regarding intragroup loans?

- What are the implications of the current increase of interest rate?

1. Back to basics, what are intragroup loans?

Intragroup loans are loans granted by one company to another company part of the same group (quite obviously). In most cases these loans are interest bearing debt.

Intragroup loans are one of the main intragroup financing instruments used by MNEs, and part of Transfer Pricing Financial Services (“TPFS”). Other intragroup financial instruments typically include cash pools, hedging contracts, derivatives, etc.

2. What are the main transfer pricing questions raised by intragroup loans?

Transfer pricing analyses of intragroup loans focus on determining whether their terms and conditions comply with the arm’s length principle. This means that the terms and conditions of an intercompany loan should not differ from those that would have been made between independent enterprises. Two main issues are the focus of transfer pricing practitioners and tax authorities:

- The interest rate and other pricing components of an intercompany loan should be set in line with market interest rates.

- Firms may finance either through equity or debt. Intragroup loans should be set so that the ratios of equity and debt of the borrower are in line with the ones of independent companies and/or remain within the limits justified by the borrower’s operational needs and financial capacity. This means that the amount of the loan should also be set at arm’s length. Companies with low equity/debt ratio are said to be thinly capitalized. Many countries have put in place specific rules to limit thinly capitalized firms.

Local tax rules will vary from one country to another, but the main tax risks faced by an MNE are:

- On the borrower side, that the interest payments are not (fully) deductible (for e.g. because tax authorities in the country of the borrower consider that the interest rate is too high).

- On the lender side, that the tax administration would add back additional interest payment to taxable income (for e.g. because tax authorities in the country of the lender consider that the interest rate is too low).

These tax risks are rendered larger by the fact that (i) most intragroup loans have long maturities, and that (ii) additional transfer pricing penalties may apply.

In recent years, new national regulations have focused on loan characteristics and adequacy beyond interest rates. In Germany, Section 1 of the " Außensteuergesetz " was updated to include paragraph 3d on internal loans and gearing adequacy.

3. Which transfer pricing methodology should I use to document intragroup loans?

Transfer pricing guidelines (most notably the OECD guidelines) set forth various methods to determine the arm’s length nature of intragroup transactions. In practice, to price intragroup loans, practitioners rely mostly on the Comparable Uncontrolled Price method (the “CUP” method). This method compares the terms and conditions of an intragroup loan with the terms and conditions of comparable financial instruments concluded between third parties.

This method is often hard to apply for intragroup services where comparable data are scarce, but, luckily, financial markets and finance theory ensure that plenty of comparable data are available to price intragroup financial instruments.

There are two ways to apply the CUP method:

- Using external data – Financial markets provide daily information on the pricing of financial instruments between independent buyers and sellers. This information can be leveraged to price intragroup loans.

- Using internal data – MNEs can also leverage information on their own third-party debt to use as evidence of acceptable pricing between third parties.

4. How should arm’s length interest rates be computed?

This section covers only the external CUP method and adheres to the OECD approach. Different approaches may be applied based on national legislation. Using the external CUP method, arm’s length interest rates are typically calculated using a two-step approach:

- The first step consists in performing a shadow credit rating of the tested instrument. This credit rating should also reflect implicit parent support: the standard approach in transfer pricing is to consider that, when a subsidiary is granted a loan, it may benefit to (some) parent support. This means that, in case of an adverse event, the parent company may decide (or not) to financially support its subsidiary. This support is usually only partial, and credit rating agencies take into account both the willingness and ability of the parent to support its subsidiary. In the end, the implicit support of the parent will impact positively the credit rating of the subsidiary.

- The second step consists in performing a yield analysis, i.e. leveraging available internal and/or external financial data to compute an arm’s length range for the interest rate. The determination of arm’s length interest rates is based on multiple factors including (but not limited to): The credit rating based on the previous analysis

- The maturity of the loan

- The country of the debtor

- The currency

5. As a taxpayer, how can I document my transfer pricing policy regarding intragroup loans?

For Transfer Pricing Financial Services, the practice is to document the arm’s length nature of each financing instrument separately.

Differences exist across jurisdictions, but you should aim at a contemporaneous documentation justifying the arm’s length nature of the transaction, and focusing in particular on the interest rate and debt / equity ratios.

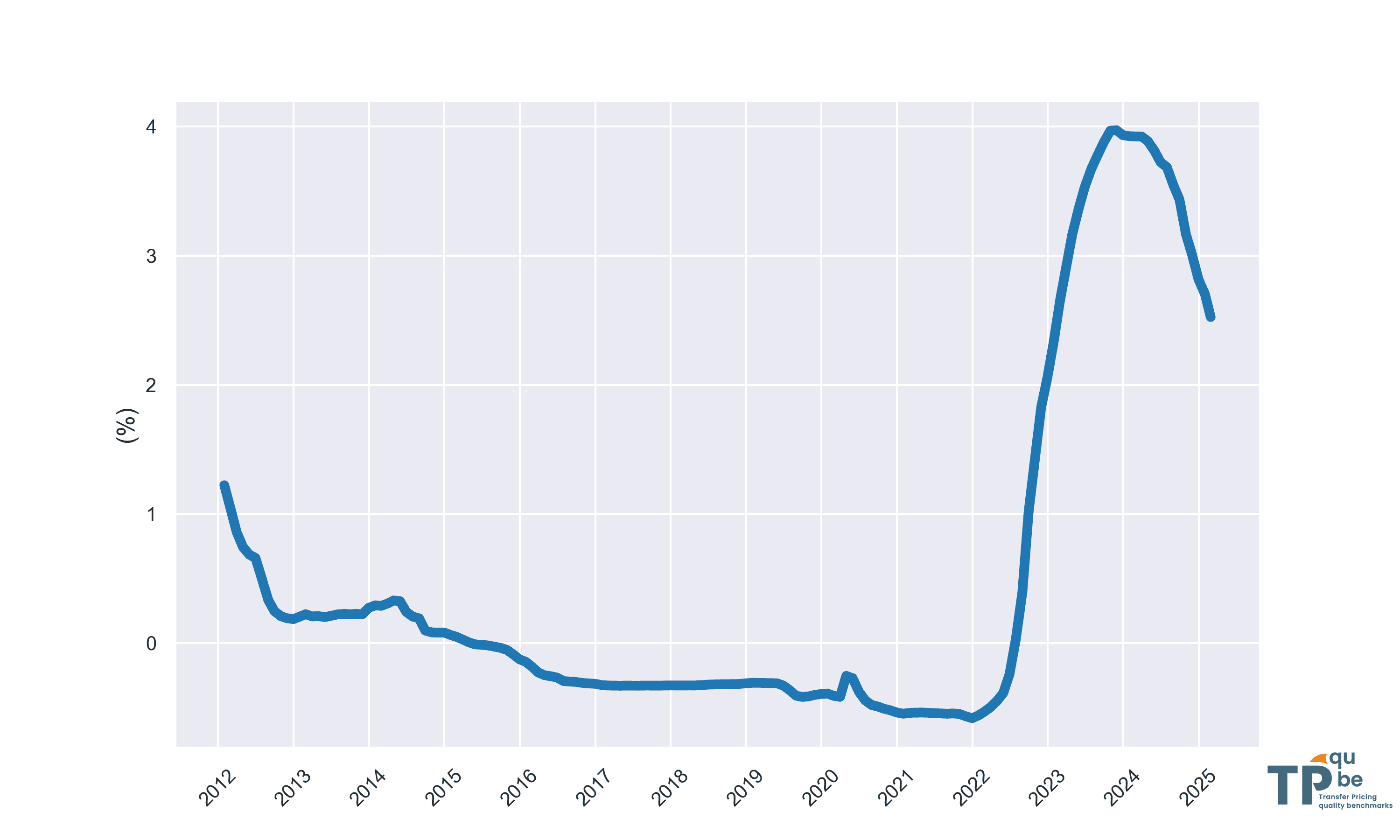

6. What are the implications of the current increase of interest rate?

After more than a decade of decrease, interest rates have increased sharply since 2022. This rise is observed in both the US and Europe and for all type of issuers. As an example, the graph on the right hand side depicts the evolution of the Euribor 12 months that is used as a reference rate in the eurozone. For tax practitioners, this means that new loans concluded in 2022 or later will have higher interest rates compared to loans concluded previously. As a result, tax impacts will be larger. Tax administrations will increase their scrutiny, notably thanks to more automatized approaches to detect loans that should be reviewed and that could lead to reassessments. Many MNEs tend to routinely renew their loans, without updating their yield analyses. These data suggest that they should revise this practice. It is important to monitor changes in legislation, as new rules can affect existing loans. For instance, the German regulation enacted on 27 March 2024 took effect on 1 January 2024 and may impact loans made before 2024. Additionally, deviations from OECD standards pose a risk of double taxation.

Euribor 12-months evolution 2012 - 2025