Tp qube

This article is the first part of our simplified guide on transfer pricing comparable company searches, with a focus on European searches. This guide aims at presenting the key features of comparable company searches to tax and finance professionals exposed to transfer pricing issues. This first article details why one would need a comparable company search, while the second one (available here) will tackle how to perform them.

In this document, we will answer the following questions:

- First thing first, what are transfer prices?

- How is the arm’s length principle applied?

- For which TP methods are comparable company searches needed?

- How to choose the tested party whose profitability will be set/tested by the search?

- Amongst transactional methods, what is the difference between the TNMM and the profit split?

- In practice, are transactional methods frequently used?

First thing first, what are transfer prices?

A transfer price is the price of a transaction between legal entities part of the same group, but located in different jurisdictions. Transfer prices may concern the sale of goods or services, the transfer or license of tangible and intangible assets, financial instruments such as guarantees or loans, etc.

The transfer price of a transaction impacts the taxable income of each party to a transaction (see graph below). As a result, states have put in place rules on how transfer prices should be determined. These rules are – mostly – based on the arm’s length principle. This principle (and its application) is stated in the “OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations”, which state in their 2017 version that: “conditions are made or imposed between the two enterprises in their commercial or financial relations which differ from those which would be made between independent enterprises, then any profits which would, but for those conditions, have accrued to one of the enterprises, but, by reason of those conditions, have not so accrued, may be included in the profits of that enterprise and taxed accordingly.”

In other words, transfer prices must be market prices.

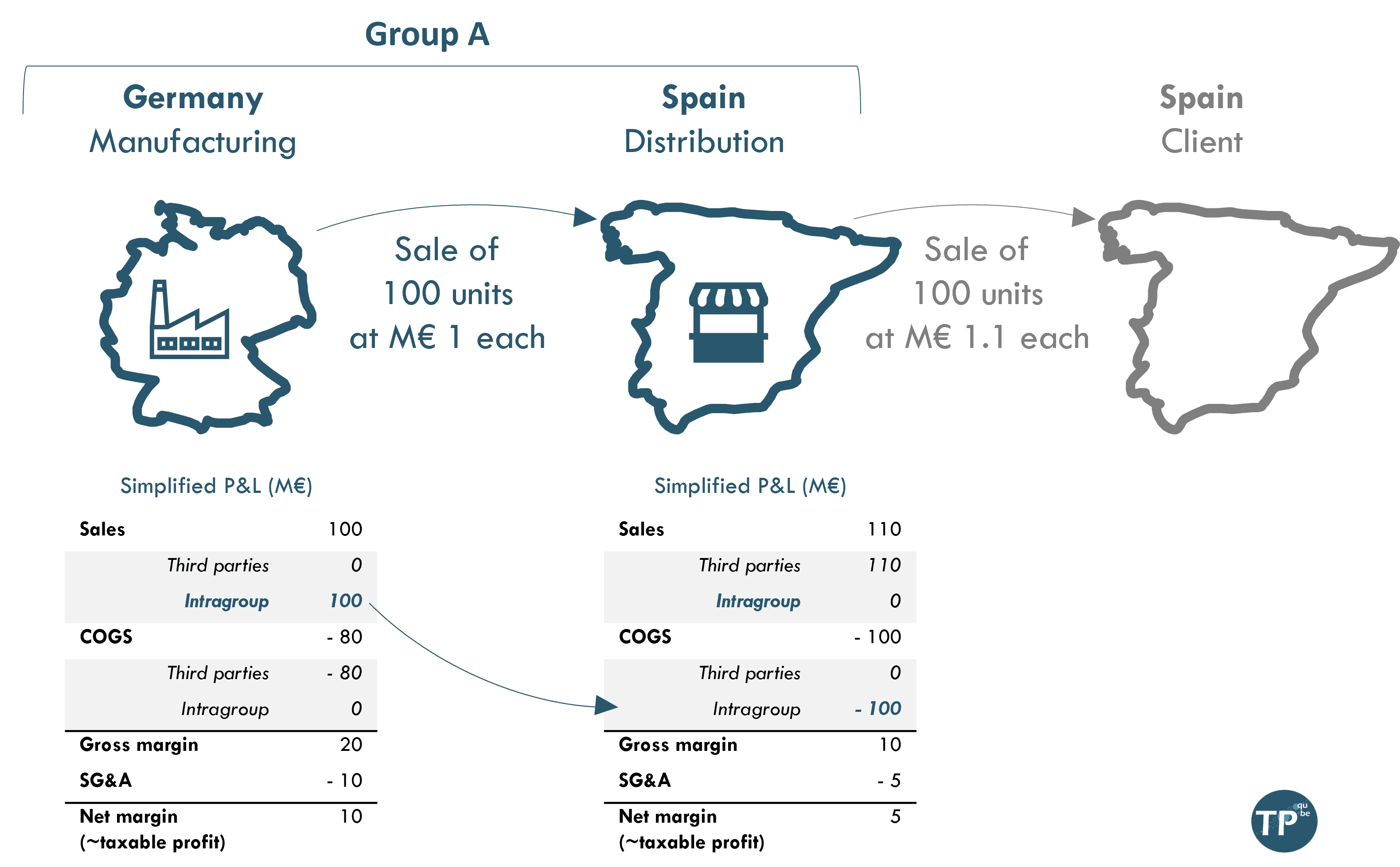

Example – A group with a subsidiary in Germany selling products to a related company in Spain. The transfer price (M€ 100) impacts the taxable profit in both countries

Understanding the legal complexity of transfer pricing

There does not exist an international convention on transfer pricing, accepted by all states throughout the globe. The principles governing transfer prices are derived from various legal sources of different values (tax treaties, domestic laws, OECD Model Tax Convention, case-law, etc.). It is thus improper to talk about global transfer pricing rules, but rather of a body of rules built around the same common principle (the arm’s length principle).

The OECD has pioneered the creation of a multilateral transfer pricing framework, and has since been leading most of the efforts to build a global consensus on these issues. The OECD Guidelines are commonly used by tax administrations and tax practitioners in many jurisdictions, and are the closest substitute to a global unified guide.

How is the arm’s length principle applied?

The OECD Guidelines distinguish two types of methods:

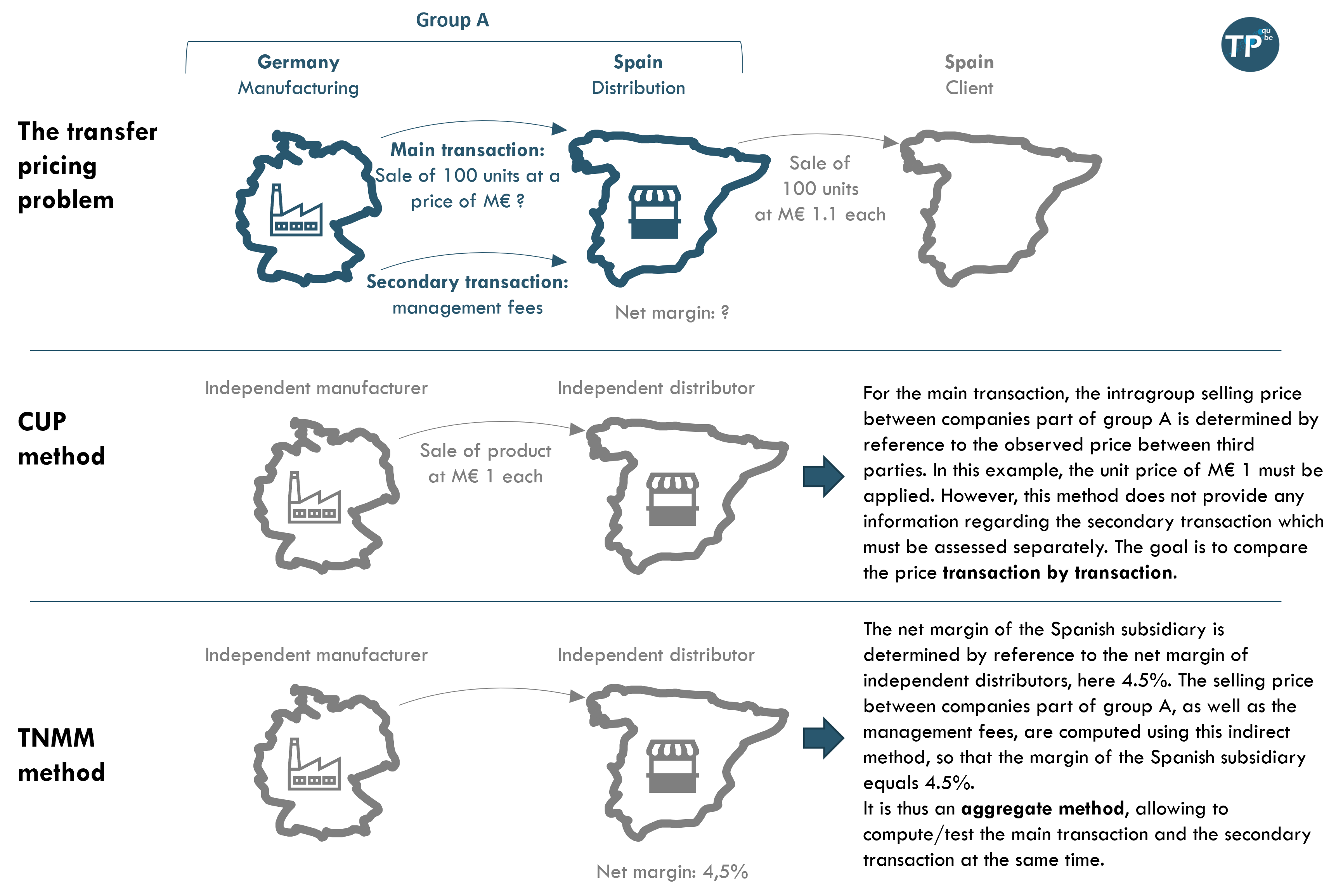

- Three traditional methods: the Comparable Uncontrolled Price method (CUP), the Resale Price method, the Cost Plus method.

- Two transactional methods: the Transactional Net Margin Method (TNMM) and the Profit Split method.

Roughly speaking, one can consider that traditional methods focus on transaction by transaction analyses, whereas transactional methods are aggregate methods, focusing on the net margin of related parties (see example below).

Application of the Comparable Uncontrolled Price method and the TNMM method

The functional analysis at the core of all transfer pricing studies aim at understanding the organization of a multinational enterprise, through the repartition of the functions, assets and risks between its legal entities and the mapping of the intragroup flows. The choice of a transfer pricing method is the outcome of the functional analysis.

For which TP methods are comparable company searches needed?

Comparable company searches (also called benchmarks) are a specific transfer pricing analysis, aiming at identifying a set of independent companies comparable to the tested party (we will go back on the exact process of comparable company searches in the second part of this guide).

Transactional methods (almost) always require to perform a comparable company search. The comparable company search will serve as an external reference point for the net margin of the testing party.

For traditional methods, comparable company searches are sometimes required, but less frequently.

How to choose the tested party whose profitability will be set/tested by the search?

Transfer pricing practitioners often rely on a useful simplification: the entrepreneur / routine framework. According to this framework, each legal entity part of an MNE can be characterized either as routine or entrepreneur. Entrepreneurs are the entities making unique and high value-added contributions for the group. They are the ones taking strategic decisions, owning the main assets (notably intangibles) and bear the main risks. Conversely, routine entities do not take strategic decisions, do not own the main assets and bear minimal risks.

In practice, it is easier to delimit the activities of routine entities and as a result to find comparable companies with a similar functional profile. Most comparable company searches are thus used to determine the normative profitability of routine entities, guaranteeing a limited margin, in line with observed market evidence.

In a group, there may exists several entrepreneur entities (then usually called co-entrepreneurs) and several routine entities.

Who is the owner of intangible assets: the DEMPE framework

The DEMPE framework is one of the outcome of the Base Erosion and Profit Shifting project (BEPS). It offers a new framework to analyze the economic ownership of intangible assets inside an MNE. In transfer pricing analyses, intangible assets are defined rather broadly and include patents, know-how, trademarks, rights under contracts, etc. Entrepreneurs are generally the owners of the main intangible assets of the group, explaining why analyzing the economic ownership of intangible assets is crucial in transfer pricing.

The DEMPE approach consists in measuring the contribution of each legal entity to the economic ownership of intangible assets within the group, by analyzing their contribution in the development, enhancement, maintenance, protection and exploitation of these intangible assets.

Among transactional methods, what is the difference between the TNMM and the profit split?

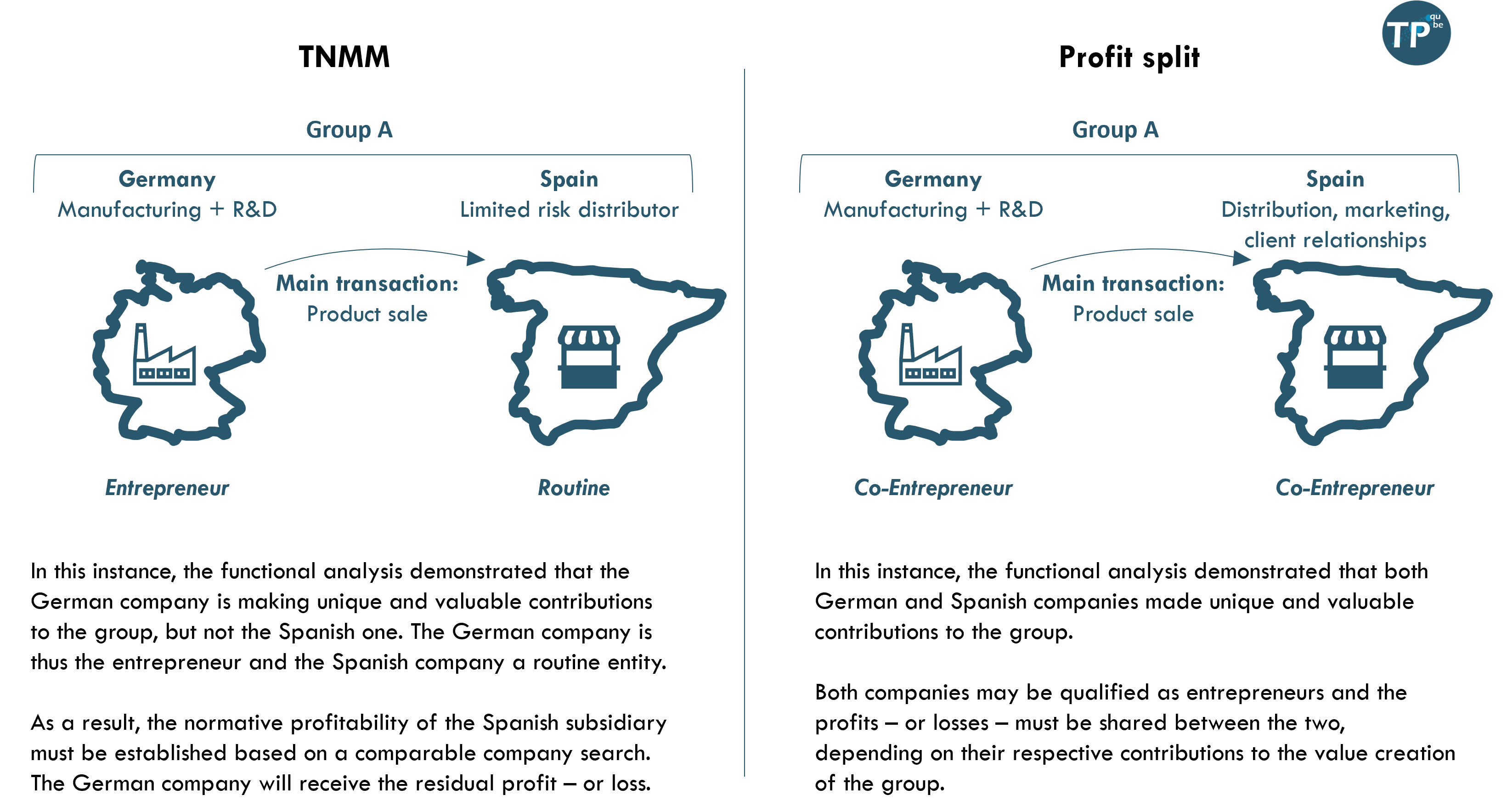

The TNMM is a “one-sided” method, applicable in the relationship between two entities, when one is an entrepreneur and the other a routine entity. In this framework, the routine entity receives a net margin determined in advance, while the entrepreneur gets the residual profit – or loss. The routine entity is thus the tested party in the comparable company search. If the group generates significant profits, they will solely benefit the entrepreneur.

Conversely, the profit split method is “double-sided”, applicable in the relationship between two entities, when both are co-entrepreneurs. In this case, the consolidated profit should be shared between the co-entrepreneurs.

A simplified example is provided below, illustrating in two close settings why the TNMM or the profit split should be chosen.

Simplified example of application of the TNMM and profit split in two close settings

In practice, are transactional methods frequently used?

Yes. The TNMM is probably the most used method by transfer pricing practitioners in Europe.

Check the second part of this guide to learn more on how to perform a comparable company search.