We released a new working paper on “The Importance of Size in Transfer Pricing Comparable Company Searches”. The full article can be found here: https://ssrn.com/abstract=3298727. We summarize below its main points and provide further guidance.*

TP qube

Motivation: Size is inconsistently treated in comparable company searches

Comparable company searches are at the core of the Transactional Net Margin Method (CPM in the US), which is the most commonly used method byTransfer Pricing practitioners. These searches are, however, a delicate exercise. As perfect comparable companies – that are similar to the tested party in all its characteristics – simply do not exist, one has to make choices and ignore some features. Consciously or not, practitioners make the hypothesis that ignored features have a limited influence on the profitability of independent companies. One feature that is all too often overlooked is the size of comparable companies.

The most common practice to deal with the size of comparable companies consists in the rejection of very small companies (typically with a turnover below 1 MEUR) and in considering that, above this threshold, size can be safely ignored. As a result, small to medium sized companies are retained (in Europe) to benchmark significantly larger subsidiaries of MNEs. The robustness of this practice is rarely tested and may lead to biased results.

Motivation: Size is inconsistently treated in comparable company searches

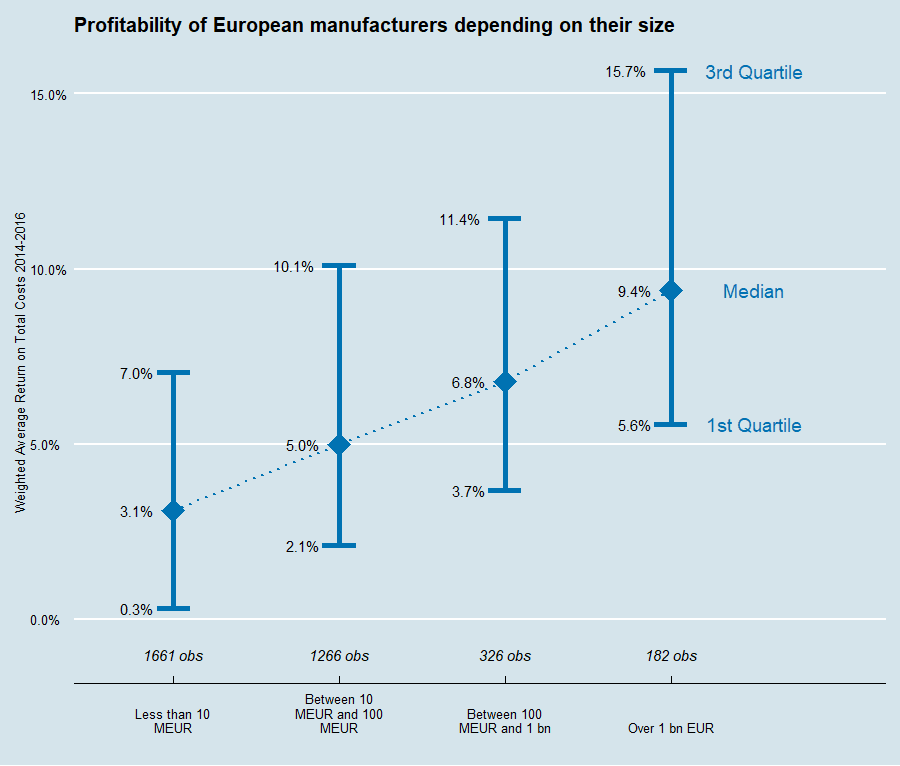

In short, we document the existence of a size premium for independent manufacturing companies in Europe: larger companies tend to have higher Return on Total Costs. Our main results are presented in the graph below:

Interquartile range of 3-year Weighted Average Return on Total Costs ( = EBIT / Total Costs) for independent European manufacturers split by turnover size in 2016

Unambiguously, independent manufacturing companies with larger size display higher profitability in Europe. This effect is of high magnitude: the median RoTC in the group with a turnover inferior to 10 MEUR is 3.1%, while the median RoTC in the group with a turnover revenue superior to 1 bn EUR is 9.4%.

Recommendations: TP qube statistical model allows to capture the impact of size in comparable company searches

Larger manufacturing companies in Europe have higher levels of profitability. Following the OECD Guidelines (2017), size should thus be systematically taken into account when performing a comparable company search in industries where such size premia are observed, in order to reinforce comparability between comparable data and the tested party. This may be done during the comparable company selection process or, after, based on comparability adjustments. The current practice of relying on small comparable companies to benchmark large MNEs should be revised.

Naturally, the next question that comes to mind is: how can one take into account these size premia in comparable company searches? We believe that predictive statistical models, pioneered by TP qube for Transfer Pricing purposes, are the best way to take size premia into account, as they allow to:

- Directly propose an estimation that takes size effects into account, or to perform size adjustments on a panel of manually selected comparable companies

- Identify size effects at the most granular level

- Disentangle the effects of size with other effects. Size is not the only critical parameter to take into account when performing comparable company searches The profitability of the company will depend on other internal and external factors, such as its geography, maturity, competition, market size, working capital policy, access to financing, and many others, that should also be captured.