TP qube

The Dutch Tax Authorities are widely recognized for their pragmatic approach notably by their willingness to engage in constructive negotiations and the number of granted Advance Pricing Agreements (APAs). APAs provide taxpayers with certainty over their tax position in one jurisdiction (or two jurisdictions in the case of bilateral agreements).

One notable feature of the Dutch APA practice is the publication of anonymized summaries. These summaries offer valuable insights into prevailing transfer pricing practices and the types of arrangements typically accepted by the authorities.

Building on our expertise in AI, we analyzed a large sample of these APA summaries to uncover key trends and patterns. As of the 656 APAs collected, it was possible to retrieve interesting insights for around two-thirds of them by leveraging a dedicated agentic workflow[1]. From the standardized information available, we were able to derive a range of statistics, some of which are illustrated below.

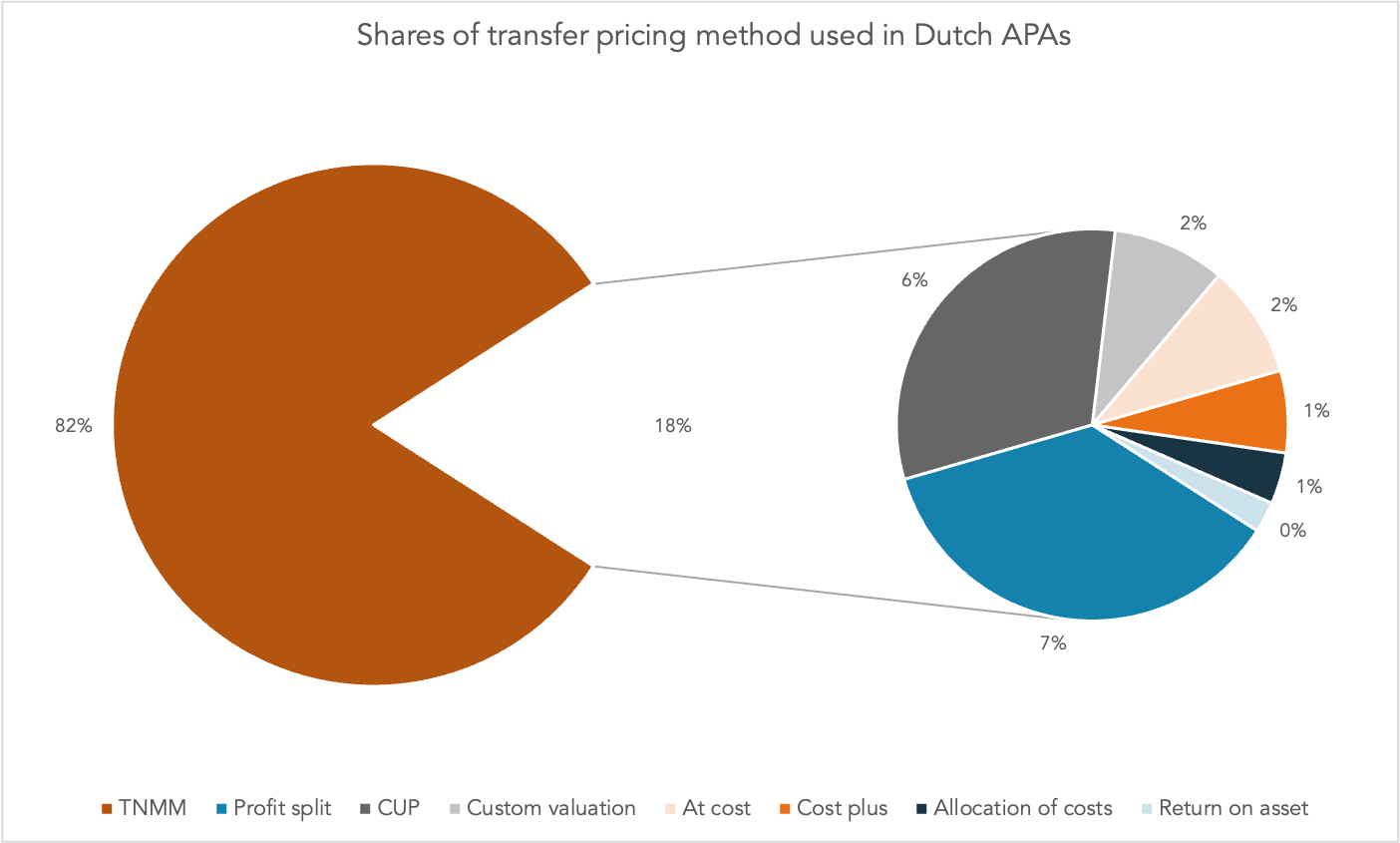

The TNMM, the Lion share of transfer pricing methods used in Dutch APAs

As shown above, the Transactional Net Margin Method (TNMM) (visually reminiscent of a Pac-Man) dominates the landscape, accounting for the largest share of methods used. Profit Split methods come in second, typically applied in cases involving highly profitable or integrated business models where securing a stable tax position is particularly valuable.

Interestingly, a small portion of APAs rely on what appear to be cost pass-through arrangements. At first glance, this may seem surprising, as such structures involve limited transfer pricing complexity. Maybe, in that case, the related fees are just invoiced at costs by the consulting firm.

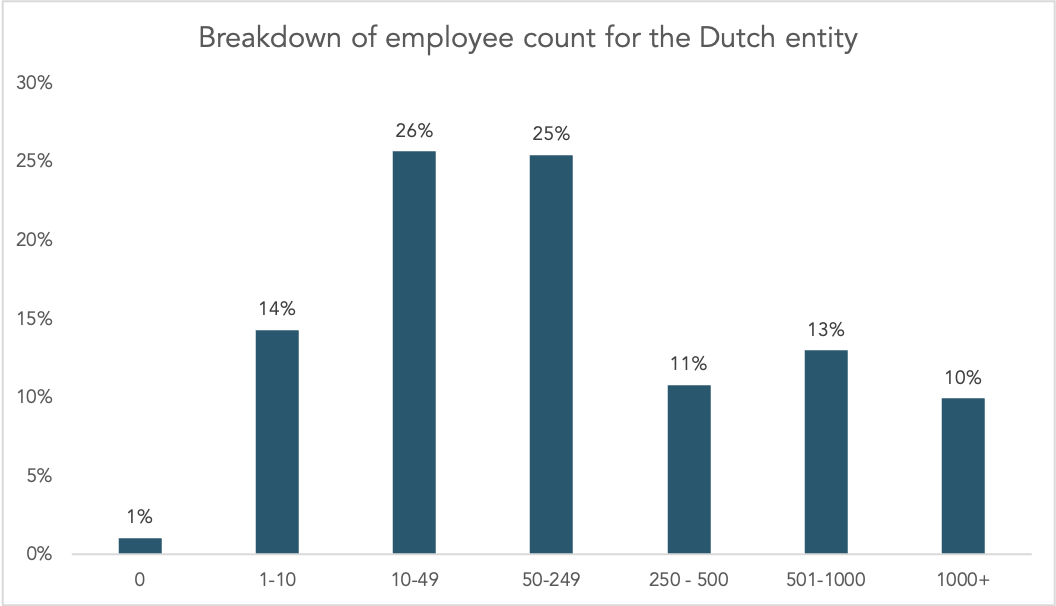

APAs are not limited to companies having important activities in the Netherlands

Another key insight relates to substance. The majority of entities covered by these APAs are relatively modest in size, with around two-thirds employing fewer than 250 people in the Netherlands.

The graph below depicts the breakdown of the number of APAs by the size (in number of employees) of the Dutch entity.

This highlights that APAs are not limited to large-scale operations but are also widely used by mid-sized structures (in the Netherlands) seeking tax certainty.

We will continue to explore the source of data, and provide interesting insight. If you’d like to explore additional findings, feel free to reach out or follow TP qube on Linkedin to be notified when we will post additional insights.

Notes:

[1]: This article remains statics and relies on data as of February 2026. We anticipate future update and additional insights.