TP qube

With the rise in interest rates since 2022 and the release of revised OCED Transfer Pricing Guidelines in 2022 including new cash pooling recommendations, we believe this is the right moment to publish this simplified guide on transfer pricing issues raised by cash pooling.

In this document, we will answer the following questions:

- What is cash pooling?

- What are the benefits of cash pooling for MNEs?

- What financial flows are typically seen in cash pool systems?

- Why are cash pools under the watchful eye of tax authorities?

- Which main factors should I take into account to make sure that my cash pool mimics an arm’s length outcome?

- Ultimately, what are the tax risks associated with cash pools?

1. What is cash pooling?

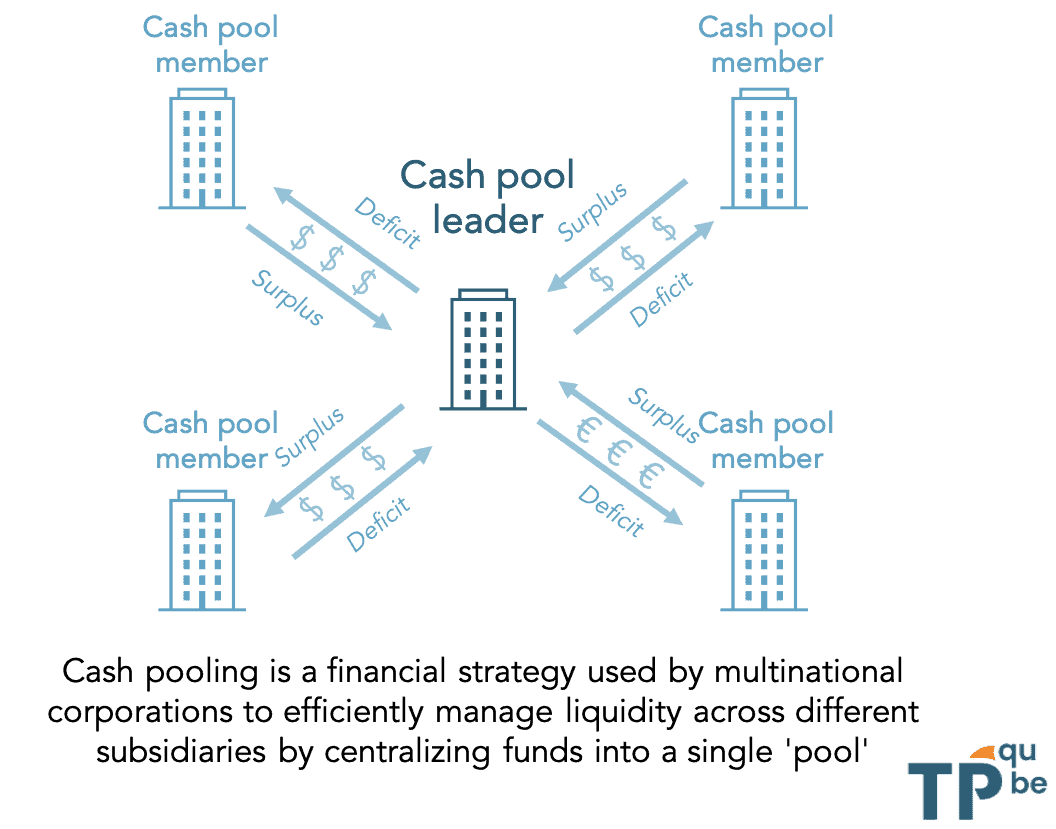

Cash pooling is a short-term financial management strategy used by multinational corporations to manage their liquidity efficiently across different subsidiaries. It's a process where funds from different subsidiaries are centralized, essentially creating a 'pool' of cash. This allows the subsidiaries with excess cash to lend to those with a deficit. Cash pool operations are generally organized with the help of a third party bank.

It helps to consider two groups of cash pool participants: (i) the cash pool leader – which is the entity centralizing the cash, and (ii) the cash pool members.

Cash pooling can come in two primary forms: physical pooling and notional pooling.

- Physical Cash Pooling: This method involves the daily active management of all participant accounts in a cash pool. Funds from accounts with surplus balances are moved to the centralized master account. Conversely, accounts with deficits are topped up to reach a target balance, utilizing the surplus funds or cash held by the cash pool leader.

- Notional Cash Pooling: This arrangement doesn't involve the physical movement of funds. Instead, the third party bank examines the balances of each participant, adjusting interest charges or payments based on the aggregate net balance.

2. What are the benefits of cash pooling for MNEs?

Cash pool systems may provide several financial benefits:

- The implementation of a cash pool reduces the need for external borrowing and the associated costs.

- Conversely, as surplus funds may be collectively invested to earn higher return, the cash pool increases investment opportunities,

- The cash pool may also help reducing other banking costs (such as administrative costs for maintaining multiple accounts).

3. What financial flows are typically seen in cash pool systems?

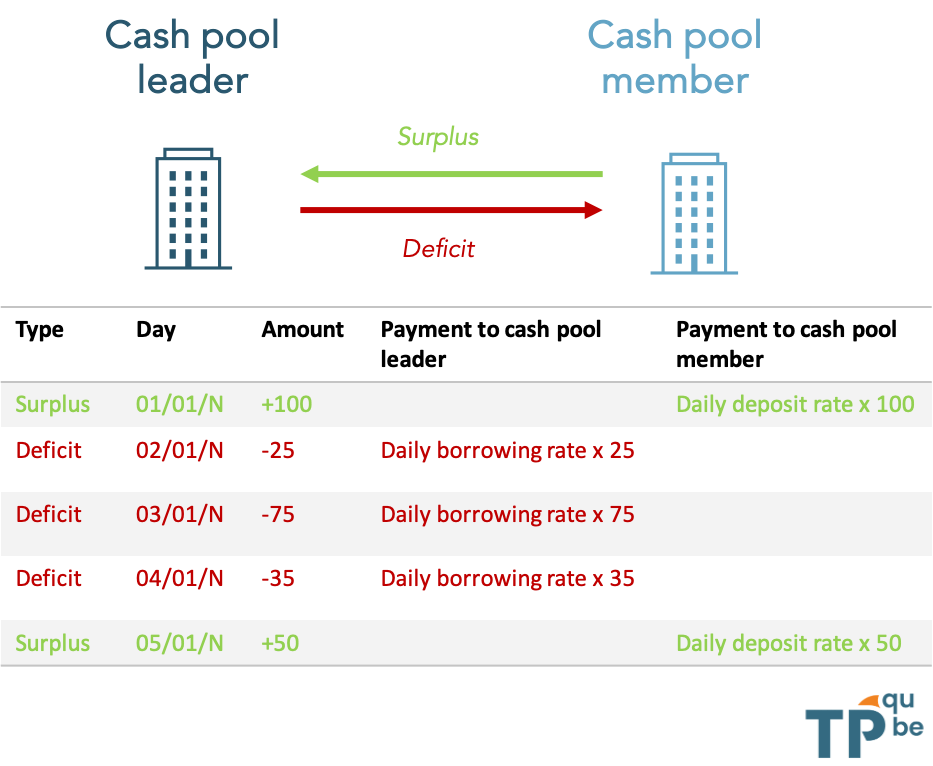

In a cash pool arrangement, the bank ensures the target balance for each participant is maintained by making the necessary transfers. Over the year, inside the cash pool, interest on the participants' balances is either charged or paid based on the terms set out in the pooling agreements.

Lump-sum payments between entities may also be performed, either to balance the cash pool system at the end of the year, or to cover certain costs.

4. Why are cash pools under the watchful eye of tax authorities?

As noted in the 2022 OECD guidelines §10.115 [1], cash pooling are not agreements observed between independent parties. This characteristic presents unique challenges in assessing the arm's length principle of a cash pool, which make certain tax authorities uneasy. In some way, as cash pooling is a widespread practice with obvious operational benefits, tax authorities are willing to authorize their existence, albeit with strict conditions (notably their sort-term nature - more on that later).

Besides, with interest rates on the rise, it's apparent that potential tax audits could result in extra gains for tax authorities, positioning cash pools as an obvious focus.

5. Which main factors should I take into account to make sure that my cash pool mimics an arm’s length outcome?

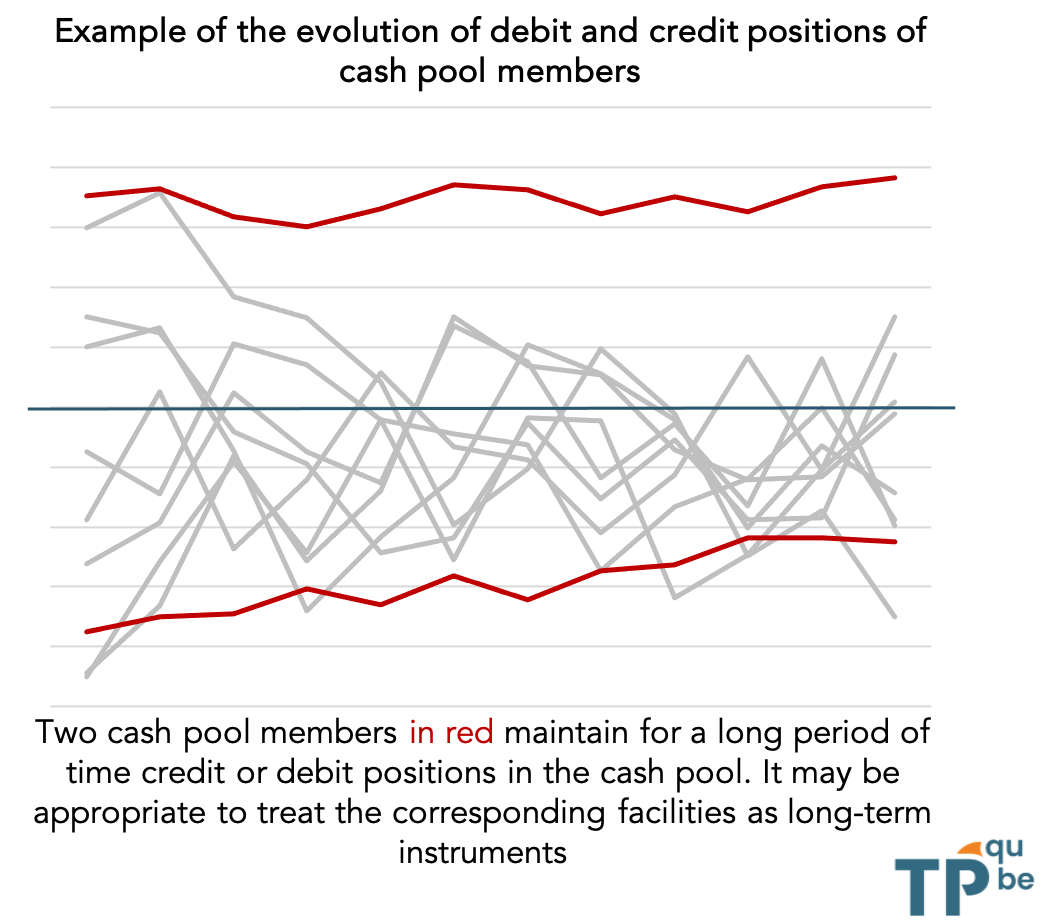

Factor 1 – Identifying long term positions in the cash pool

Cash pools are only authorized as long as they are short-term liquidity arrangements. It may be that certain members of the cash pool maintain for a long period of time credit or debit positions in the cash pool. In most cases, it is appropriate to treat the corresponding facilities as long-term instruments, such as long-term term loans or deposits.

Factor 2 – Pricing of borrowing and lending interest rates

Quite evidently, borrowing and lending interest rates should be determined by reference to market evidence. Credit risk is inherent to cash pooling, as some cash pool members may not be in a capacity to repay their debts.

In an ideal setting, all cash pool members would thus need to be attributed a credit rating to capture their differences in credit risks, translating in different borrowing interest rates. This approach is however and not always practical to implement.

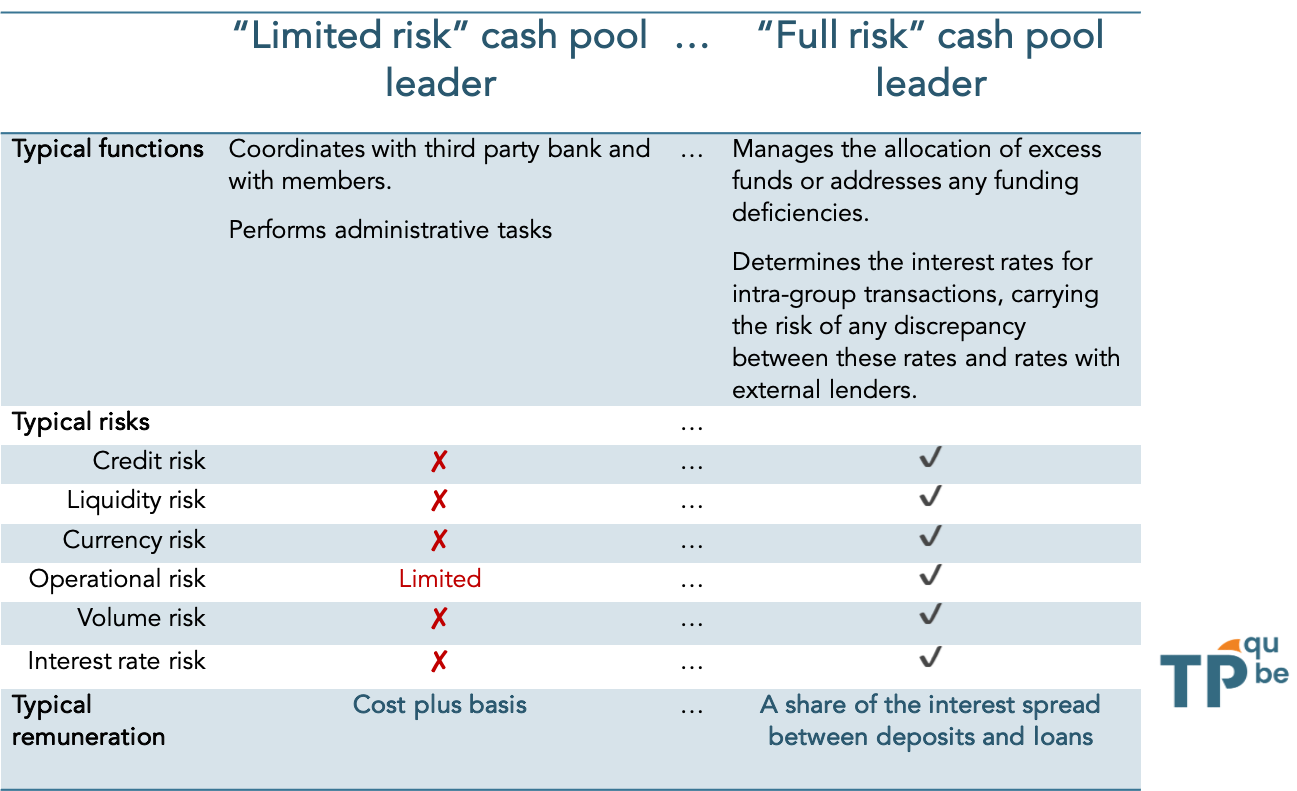

Factor 3 – Remunerating the cash pool leader depending on its functional profile

The remuneration of the cash pool leader will heavily depend on its functional profile. This role can be seen as existing on a spectrum, with its extremes being defined as follows:

Factor 4 – Synergies

Part of the benefit of a cash pool (due to financial opportunities or operational efficiencies - see above) can be considered as arising from group synergies, i.e. incidental benefits attributable solely to its being part of a larger concern. These group synergies should be allocated among cash pool members.

6. Ultimately, what are the tax risks associated with cash pools?

There are typically three main risks associated with cash pools:

- Risks on the level of interest rates. On the borrower side, interest payments may not be fully deductible (for e.g. because tax authorities in the country of the borrower consider that the interest rate is too high). On the lender side, tax administration may add back additional interest payment to taxable income (for e.g. because tax authorities in the country of the lender consider that the interest rate is too low).

- Risks on the reclassification of the cash pool as a long-term loan. The cash pool may be treated as a long term loan by certain tax authorities, notably if the net position of a member does not vary over time. This typically means that tax authorities may consider that the interest rates paid by the borrowing side should be higher (to match the longer maturity of the financial instrument, but also because credit scores tend to be reassessed during the audit). This effect can be particularly large, sometimes increasing interest rates by hundreds of basis points.

- Risks on the reclassification of the cash pool as equity.

These risks concern first the cash pool leader but also any of the cash pool members. With more widespread tax information exchanges, increased pressure on government budget, higher interest rate and intensive usage of datamining tools it should be no surprise that cash pools are now reviewed more systematically by tax authorities.

[1] OCDE (2022), OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations 2022, Éditions OCDE, Paris, https://doi.org/10.1787/0e655865-en.